Multiple Stock Trading¶

Deep Reinforcement Learning for Stock Trading from Scratch: Multiple Stock Trading

Tip

Run the code step by step at Google Colab.

Step 1: Preparation¶

Step 1.1: Overview

To begin with, I would like explain the logic of multiple stock trading using Deep Reinforcement Learning.

We use Dow 30 constituents as an example throughout this article, because those are the most popular stocks.

A lot of people are terrified by the word “Deep Reinforcement Learning”, actually, you can just treat it as a “Smart AI” or “Smart Stock Trader” or “R2-D2 Trader” if you want, and just use it.

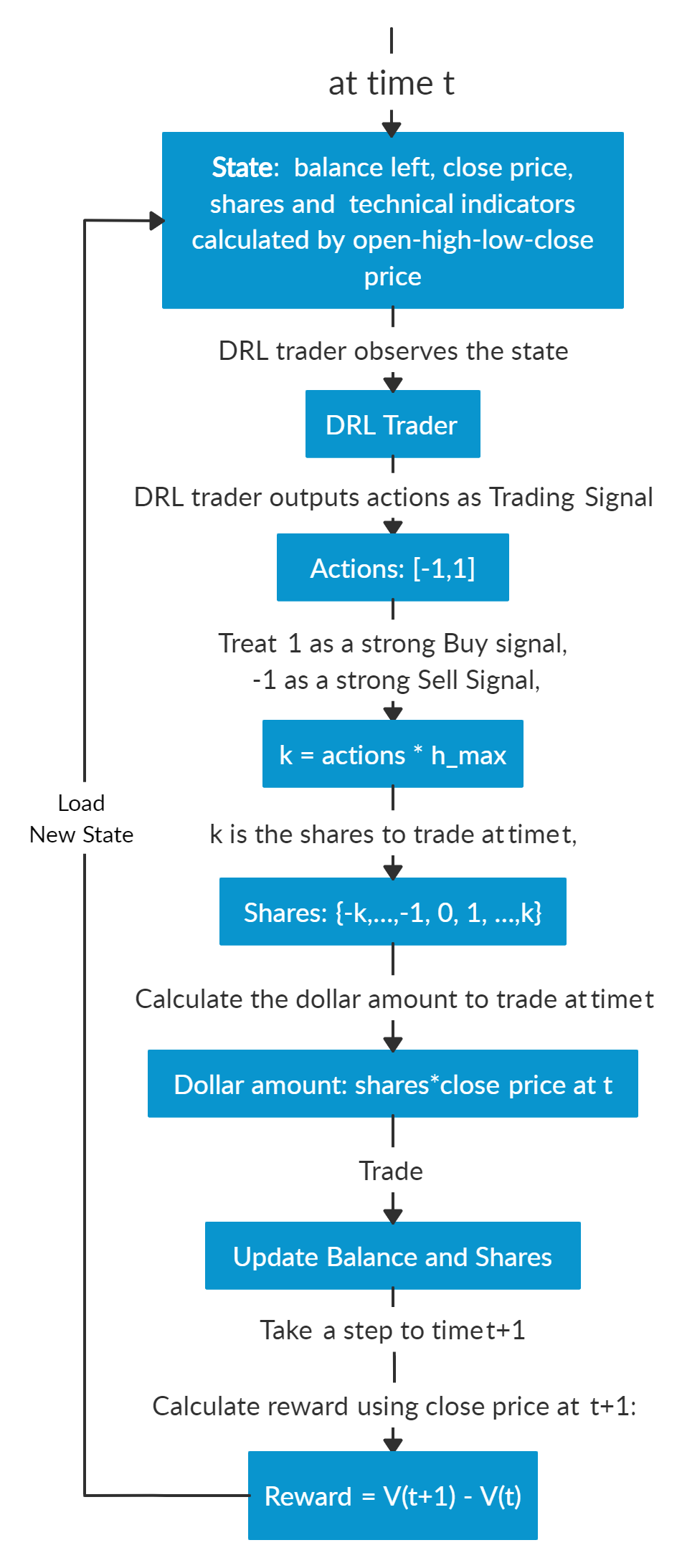

Suppose that we have a well trained DRL agent “DRL Trader”, we want to use it to trade multiple stocks in our portfolio.

Assume we are at time t, at the end of day at time t, we will know the open-high-low-close price of the Dow 30 constituents stocks. We can use these information to calculate technical indicators such as MACD, RSI, CCI, ADX. In Reinforcement Learning we call these data or features as “states”.

We know that our portfolio value V(t) = balance (t) + dollar amount of the stocks (t).

We feed the states into our well trained DRL Trader, the trader will output a list of actions, the action for each stock is a value within [-1, 1], we can treat this value as the trading signal, 1 means a strong buy signal, -1 means a strong sell signal.

We calculate k = actions *h_max, h_max is a predefined parameter that sets as the maximum amount of shares to trade. So we will have a list of shares to trade.

The dollar amount of shares = shares to trade* close price (t).

Update balance and shares. These dollar amount of shares are the money we need to trade at time t. The updated balance = balance (t) −amount of money we pay to buy shares +amount of money we receive to sell shares. The updated shares = shares held (t) −shares to sell +shares to buy.

So we take actions to trade based on the advice of our DRL Trader at the end of day at time t (time t’s close price equals time t+1’s open price). We hope that we will benefit from these actions by the end of day at time t+1.

Take a step to time t+1, at the end of day, we will know the close price at t+1, the dollar amount of the stocks (t+1)= sum(updated shares * close price (t+1)). The portfolio value V(t+1)=balance (t+1) + dollar amount of the stocks (t+1).

So the step reward by taking the actions from DRL Trader at time t to t+1 is r = v(t+1) − v(t). The reward can be positive or negative in the training stage. But of course, we need a positive reward in trading to say that our DRL Trader is effective.

Repeat this process until termination.

Below are the logic chart of multiple stock trading and a made-up example for demonstration purpose:

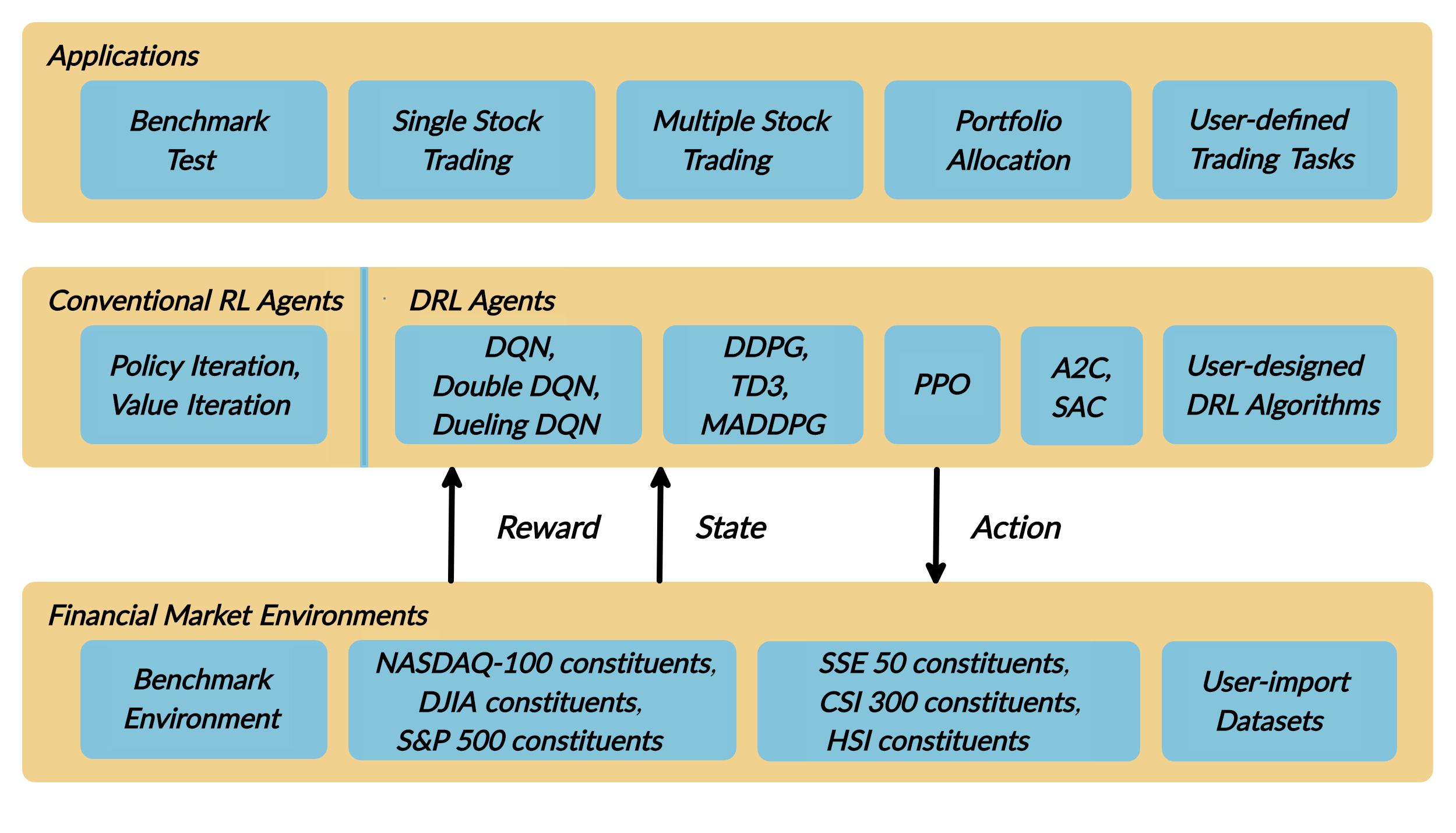

Multiple stock trading is different from single stock trading because as the number of stocks increase, the dimension of the data will increase, the state and action space in reinforcement learning will grow exponentially. So stability and reproducibility are very essential here.

We introduce a DRL library FinRL that facilitates beginners to expose themselves to quantitative finance and to develop their own stock trading strategies.

FinRL is characterized by its reproducibility, scalability, simplicity, applicability and extendibility.

This article is focusing on one of the use cases in our paper: Mutiple Stock Trading. We use one Jupyter notebook to include all the necessary steps.

Step 1.2: Problem Definition:

This problem is to design an automated solution for stock trading. We model the stock trading process as a Markov Decision Process (MDP). We then formulate our trading goal as a maximization problem. The algorithm is trained using Deep Reinforcement Learning (DRL) algorithms and the components of the reinforcement learning environment are:

Action: The action space describes the allowed actions that the agent interacts with the environment. Normally, a ∈ A includes three actions: a ∈ {−1, 0, 1}, where −1, 0, 1 represent selling, holding, and buying one stock. Also, an action can be carried upon multiple shares. We use an action space {−k, …, −1, 0, 1, …, k}, where k denotes the number of shares. For example, “Buy 10 shares of AAPL” or “Sell 10 shares of AAPL” are 10 or −10, respectively

Reward function: r(s, a, s′) is the incentive mechanism for an agent to learn a better action. The change of the portfolio value when action a is taken at state s and arriving at new state s’, i.e., r(s, a, s′) = v′ − v, where v′ and v represent the portfolio values at state s′ and s, respectively

State: The state space describes the observations that the agent receives from the environment. Just as a human trader needs to analyze various information before executing a trade, so our trading agent observes many different features to better learn in an interactive environment.

Environment: Dow 30 constituents

The data of the stocks for this case study is obtained from Yahoo Finance API. The data contains Open-High-Low-Close price and volume.

Step 1.3: FinRL installation:

1## install finrl library

2!pip install git+https://github.com/AI4Finance-LLC/FinRL-Library.git

Then we import the packages needed for this demonstration.

Step 1.4: Import packages:

1import pandas as pd

2import numpy as np

3import matplotlib

4import matplotlib.pyplot as plt

5# matplotlib.use('Agg')

6import datetime

7

8%matplotlib inline

9from finrl import config

10from finrl import config_tickers

11from finrl.finrl_meta.preprocessor.yahoodownloader import YahooDownloader

12from finrl.finrl_meta.preprocessor.preprocessors import FeatureEngineer, data_split

13from finrl.finrl_meta.env_stock_trading.env_stocktrading import StockTradingEnv

14from finrl.agents.stablebaselines3.models import DRLAgent

15

16from finrl.plot import backtest_stats, backtest_plot, get_daily_return, get_baseline

17from pprint import pprint

18

19import sys

20sys.path.append("../FinRL-Library")

21

22import itertools

Finally, create folders for storage.

Step 1.5: Create folders:

1import os

2if not os.path.exists("./" + config.DATA_SAVE_DIR):

3 os.makedirs("./" + config.DATA_SAVE_DIR)

4if not os.path.exists("./" + config.TRAINED_MODEL_DIR):

5 os.makedirs("./" + config.TRAINED_MODEL_DIR)

6if not os.path.exists("./" + config.TENSORBOARD_LOG_DIR):

7 os.makedirs("./" + config.TENSORBOARD_LOG_DIR)

8if not os.path.exists("./" + config.RESULTS_DIR):

9 os.makedirs("./" + config.RESULTS_DIR)

Then all the preparation work are done. We can start now!

Step 2: Download Data¶

Before training our DRL agent, we need to get the historical data of DOW30 stocks first. Here we use the data from Yahoo! Finance. Yahoo! Finance is a website that provides stock data, financial news, financial reports, etc. All the data provided by Yahoo Finance is free. yfinance is an open-source library that provides APIs to download data from Yahoo! Finance. We will use this package to download data here.

FinRL uses a YahooDownloader class to extract data.

class YahooDownloader:

"""

Provides methods for retrieving daily stock data from Yahoo Finance API

Attributes

----------

start_date : str

start date of the data (modified from config.py)

end_date : str

end date of the data (modified from config.py)

ticker_list : list

a list of stock tickers (modified from config.py)

Methods

-------

fetch_data()

Fetches data from yahoo API

"""

Download and save the data in a pandas DataFrame:

1 # Download and save the data in a pandas DataFrame:

2 df = YahooDownloader(start_date = '2009-01-01',

3 end_date = '2020-09-30',

4 ticker_list = config_tickers.DOW_30_TICKER).fetch_data()

5

6 print(df.sort_values(['date','tic'],ignore_index=True).head(30))

Step 3: Preprocess Data¶

Data preprocessing is a crucial step for training a high quality machine learning model. We need to check for missing data and do feature engineering in order to convert the data into a model-ready state.

Step 3.1: Check missing data

1# check missing data

2dow_30.isnull().values.any()

Step 3.2: Add technical indicators

In practical trading, various information needs to be taken into account, for example the historical stock prices, current holding shares, technical indicators, etc. In this article, we demonstrate two trend-following technical indicators: MACD and RSI.

1def add_technical_indicator(df):

2 """

3 calcualte technical indicators

4 use stockstats package to add technical inidactors

5 :param data: (df) pandas dataframe

6 :return: (df) pandas dataframe

7 """

8 stock = Sdf.retype(df.copy())

9 stock['close'] = stock['adjcp']

10 unique_ticker = stock.tic.unique()

11

12 macd = pd.DataFrame()

13 rsi = pd.DataFrame()

14

15 #temp = stock[stock.tic == unique_ticker[0]]['macd']

16 for i in range(len(unique_ticker)):

17 ## macd

18 temp_macd = stock[stock.tic == unique_ticker[i]]['macd']

19 temp_macd = pd.DataFrame(temp_macd)

20 macd = macd.append(temp_macd, ignore_index=True)

21 ## rsi

22 temp_rsi = stock[stock.tic == unique_ticker[i]]['rsi_30']

23 temp_rsi = pd.DataFrame(temp_rsi)

24 rsi = rsi.append(temp_rsi, ignore_index=True)

25

26 df['macd'] = macd

27 df['rsi'] = rsi

28 return df

Step 3.3: Add turbulence index

Risk-aversion reflects whether an investor will choose to preserve the capital. It also influences one’s trading strategy when facing different market volatility level.

To control the risk in a worst-case scenario, such as financial crisis of 2007–2008, FinRL employs the financial turbulence index that measures extreme asset price fluctuation.

1def add_turbulence(df):

2 """

3 add turbulence index from a precalcualted dataframe

4 :param data: (df) pandas dataframe

5 :return: (df) pandas dataframe

6 """

7 turbulence_index = calcualte_turbulence(df)

8 df = df.merge(turbulence_index, on='datadate')

9 df = df.sort_values(['datadate','tic']).reset_index(drop=True)

10 return df

11

12

13

14def calcualte_turbulence(df):

15 """calculate turbulence index based on dow 30"""

16 # can add other market assets

17

18 df_price_pivot=df.pivot(index='datadate', columns='tic', values='adjcp')

19 unique_date = df.datadate.unique()

20 # start after a year

21 start = 252

22 turbulence_index = [0]*start

23 #turbulence_index = [0]

24 count=0

25 for i in range(start,len(unique_date)):

26 current_price = df_price_pivot[df_price_pivot.index == unique_date[i]]

27 hist_price = df_price_pivot[[n in unique_date[0:i] for n in df_price_pivot.index ]]

28 cov_temp = hist_price.cov()

29 current_temp=(current_price - np.mean(hist_price,axis=0))

30 temp = current_temp.values.dot(np.linalg.inv(cov_temp)).dot(current_temp.values.T)

31 if temp>0:

32 count+=1

33 if count>2:

34 turbulence_temp = temp[0][0]

35 else:

36 #avoid large outlier because of the calculation just begins

37 turbulence_temp=0

38 else:

39 turbulence_temp=0

40 turbulence_index.append(turbulence_temp)

41

42

43 turbulence_index = pd.DataFrame({'datadate':df_price_pivot.index,

44 'turbulence':turbulence_index})

45 return turbulence_index

Step 3.4 Feature Engineering

FinRL uses a FeatureEngineer class to preprocess data.

Perform Feature Engineering:

1 # Perform Feature Engineering:

2 df = FeatureEngineer(df.copy(),

3 use_technical_indicator=True,

4 tech_indicator_list = config.INDICATORS,

5 use_turbulence=True,

6 user_defined_feature = False).preprocess_data()

Step 4: Design Environment¶

Considering the stochastic and interactive nature of the automated stock trading tasks, a financial task is modeled as a Markov Decision Process (MDP) problem. The training process involves observing stock price change, taking an action and reward’s calculation to have the agent adjusting its strategy accordingly. By interacting with the environment, the trading agent will derive a trading strategy with the maximized rewards as time proceeds.

Our trading environments, based on OpenAI Gym framework, simulate live stock markets with real market data according to the principle of time-driven simulation.

The action space describes the allowed actions that the agent interacts with the environment. Normally, action a includes three actions: {-1, 0, 1}, where -1, 0, 1 represent selling, holding, and buying one share. Also, an action can be carried upon multiple shares. We use an action space {-k,…,-1, 0, 1, …, k}, where k denotes the number of shares to buy and -k denotes the number of shares to sell. For example, “Buy 10 shares of AAPL” or “Sell 10 shares of AAPL” are 10 or -10, respectively. The continuous action space needs to be normalized to [-1, 1], since the policy is defined on a Gaussian distribution, which needs to be normalized and symmetric.

Step 4.1: Environment for Training

1## Environment for Training

2import numpy as np

3import pandas as pd

4from gym.utils import seeding

5import gym

6from gym import spaces

7import matplotlib

8matplotlib.use('Agg')

9import matplotlib.pyplot as plt

10

11# shares normalization factor

12# 100 shares per trade

13HMAX_NORMALIZE = 100

14# initial amount of money we have in our account

15INITIAL_ACCOUNT_BALANCE=1000000

16# total number of stocks in our portfolio

17STOCK_DIM = 30

18# transaction fee: 1/1000 reasonable percentage

19TRANSACTION_FEE_PERCENT = 0.001

20

21REWARD_SCALING = 1e-4

22

23

24class StockEnvTrain(gym.Env):

25 """A stock trading environment for OpenAI gym"""

26 metadata = {'render.modes': ['human']}

27

28 def __init__(self, df,day = 0):

29 #super(StockEnv, self).__init__()

30 self.day = day

31 self.df = df

32

33 # action_space normalization and shape is STOCK_DIM

34 self.action_space = spaces.Box(low = -1, high = 1,shape = (STOCK_DIM,))

35 # Shape = 181: [Current Balance]+[prices 1-30]+[owned shares 1-30]

36 # +[macd 1-30]+ [rsi 1-30] + [cci 1-30] + [adx 1-30]

37 self.observation_space = spaces.Box(low=0, high=np.inf, shape = (121,))

38 # load data from a pandas dataframe

39 self.data = self.df.loc[self.day,:]

40 self.terminal = False

41 # initalize state

42 self.state = [INITIAL_ACCOUNT_BALANCE] + \

43 self.data.adjcp.values.tolist() + \

44 [0]*STOCK_DIM + \

45 self.data.macd.values.tolist() + \

46 self.data.rsi.values.tolist()

47 #self.data.cci.values.tolist() + \

48 #self.data.adx.values.tolist()

49 # initialize reward

50 self.reward = 0

51 self.cost = 0

52 # memorize all the total balance change

53 self.asset_memory = [INITIAL_ACCOUNT_BALANCE]

54 self.rewards_memory = []

55 self.trades = 0

56 self._seed()

57

58 def _sell_stock(self, index, action):

59 # perform sell action based on the sign of the action

60 if self.state[index+STOCK_DIM+1] > 0:

61 #update balance

62 self.state[0] += \

63 self.state[index+1]*min(abs(action),self.state[index+STOCK_DIM+1]) * \

64 (1- TRANSACTION_FEE_PERCENT)

65

66 self.state[index+STOCK_DIM+1] -= min(abs(action), self.state[index+STOCK_DIM+1])

67 self.cost +=self.state[index+1]*min(abs(action),self.state[index+STOCK_DIM+1]) * \

68 TRANSACTION_FEE_PERCENT

69 self.trades+=1

70 else:

71 pass

72

73 def _buy_stock(self, index, action):

74 # perform buy action based on the sign of the action

75 available_amount = self.state[0] // self.state[index+1]

76 # print('available_amount:{}'.format(available_amount))

77

78 #update balance

79 self.state[0] -= self.state[index+1]*min(available_amount, action)* \

80 (1+ TRANSACTION_FEE_PERCENT)

81

82 self.state[index+STOCK_DIM+1] += min(available_amount, action)

83

84 self.cost+=self.state[index+1]*min(available_amount, action)* \

85 TRANSACTION_FEE_PERCENT

86 self.trades+=1

87

88 def step(self, actions):

89 # print(self.day)

90 self.terminal = self.day >= len(self.df.index.unique())-1

91 # print(actions)

92

93 if self.terminal:

94 plt.plot(self.asset_memory,'r')

95 plt.savefig('account_value_train.png')

96 plt.close()

97 end_total_asset = self.state[0]+ \

98 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):(STOCK_DIM*2+1)]))

99 print("previous_total_asset:{}".format(self.asset_memory[0]))

100

101 print("end_total_asset:{}".format(end_total_asset))

102 df_total_value = pd.DataFrame(self.asset_memory)

103 df_total_value.to_csv('account_value_train.csv')

104 print("total_reward:{}".format(self.state[0]+sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):61]))- INITIAL_ACCOUNT_BALANCE ))

105 print("total_cost: ", self.cost)

106 print("total_trades: ", self.trades)

107 df_total_value.columns = ['account_value']

108 df_total_value['daily_return']=df_total_value.pct_change(1)

109 sharpe = (252**0.5)*df_total_value['daily_return'].mean()/ \

110 df_total_value['daily_return'].std()

111 print("Sharpe: ",sharpe)

112 print("=================================")

113 df_rewards = pd.DataFrame(self.rewards_memory)

114 df_rewards.to_csv('account_rewards_train.csv')

115

116 return self.state, self.reward, self.terminal,{}

117

118 else:

119 actions = actions * HMAX_NORMALIZE

120

121 begin_total_asset = self.state[0]+ \

122 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):61]))

123 #print("begin_total_asset:{}".format(begin_total_asset))

124

125 argsort_actions = np.argsort(actions)

126

127 sell_index = argsort_actions[:np.where(actions < 0)[0].shape[0]]

128 buy_index = argsort_actions[::-1][:np.where(actions > 0)[0].shape[0]]

129

130 for index in sell_index:

131 # print('take sell action'.format(actions[index]))

132 self._sell_stock(index, actions[index])

133

134 for index in buy_index:

135 # print('take buy action: {}'.format(actions[index]))

136 self._buy_stock(index, actions[index])

137

138 self.day += 1

139 self.data = self.df.loc[self.day,:]

140 #load next state

141 # print("stock_shares:{}".format(self.state[29:]))

142 self.state = [self.state[0]] + \

143 self.data.adjcp.values.tolist() + \

144 list(self.state[(STOCK_DIM+1):61]) + \

145 self.data.macd.values.tolist() + \

146 self.data.rsi.values.tolist()

147

148 end_total_asset = self.state[0]+ \

149 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):61]))

150

151 #print("end_total_asset:{}".format(end_total_asset))

152

153 self.reward = end_total_asset - begin_total_asset

154 self.rewards_memory.append(self.reward)

155

156 self.reward = self.reward * REWARD_SCALING

157 # print("step_reward:{}".format(self.reward))

158

159 self.asset_memory.append(end_total_asset)

160

161

162 return self.state, self.reward, self.terminal, {}

163

164 def reset(self):

165 self.asset_memory = [INITIAL_ACCOUNT_BALANCE]

166 self.day = 0

167 self.data = self.df.loc[self.day,:]

168 self.cost = 0

169 self.trades = 0

170 self.terminal = False

171 self.rewards_memory = []

172 #initiate state

173 self.state = [INITIAL_ACCOUNT_BALANCE] + \

174 self.data.adjcp.values.tolist() + \

175 [0]*STOCK_DIM + \

176 self.data.macd.values.tolist() + \

177 self.data.rsi.values.tolist()

178 return self.state

179

180 def render(self, mode='human'):

181 return self.state

182

183 def _seed(self, seed=None):

184 self.np_random, seed = seeding.np_random(seed)

185 return [seed]

Step 4.2: Environment for Trading

1## Environment for Trading

2import numpy as np

3import pandas as pd

4from gym.utils import seeding

5import gym

6from gym import spaces

7import matplotlib

8matplotlib.use('Agg')

9import matplotlib.pyplot as plt

10

11# shares normalization factor

12# 100 shares per trade

13HMAX_NORMALIZE = 100

14# initial amount of money we have in our account

15INITIAL_ACCOUNT_BALANCE=1000000

16# total number of stocks in our portfolio

17STOCK_DIM = 30

18# transaction fee: 1/1000 reasonable percentage

19TRANSACTION_FEE_PERCENT = 0.001

20

21# turbulence index: 90-150 reasonable threshold

22#TURBULENCE_THRESHOLD = 140

23REWARD_SCALING = 1e-4

24

25class StockEnvTrade(gym.Env):

26 """A stock trading environment for OpenAI gym"""

27 metadata = {'render.modes': ['human']}

28

29 def __init__(self, df,day = 0,turbulence_threshold=140):

30 #super(StockEnv, self).__init__()

31 #money = 10 , scope = 1

32 self.day = day

33 self.df = df

34 # action_space normalization and shape is STOCK_DIM

35 self.action_space = spaces.Box(low = -1, high = 1,shape = (STOCK_DIM,))

36 # Shape = 181: [Current Balance]+[prices 1-30]+[owned shares 1-30]

37 # +[macd 1-30]+ [rsi 1-30] + [cci 1-30] + [adx 1-30]

38 self.observation_space = spaces.Box(low=0, high=np.inf, shape = (121,))

39 # load data from a pandas dataframe

40 self.data = self.df.loc[self.day,:]

41 self.terminal = False

42 self.turbulence_threshold = turbulence_threshold

43 # initalize state

44 self.state = [INITIAL_ACCOUNT_BALANCE] + \

45 self.data.adjcp.values.tolist() + \

46 [0]*STOCK_DIM + \

47 self.data.macd.values.tolist() + \

48 self.data.rsi.values.tolist()

49

50 # initialize reward

51 self.reward = 0

52 self.turbulence = 0

53 self.cost = 0

54 self.trades = 0

55 # memorize all the total balance change

56 self.asset_memory = [INITIAL_ACCOUNT_BALANCE]

57 self.rewards_memory = []

58 self.actions_memory=[]

59 self.date_memory=[]

60 self._seed()

61

62

63 def _sell_stock(self, index, action):

64 # perform sell action based on the sign of the action

65 if self.turbulence<self.turbulence_threshold:

66 if self.state[index+STOCK_DIM+1] > 0:

67 #update balance

68 self.state[0] += \

69 self.state[index+1]*min(abs(action),self.state[index+STOCK_DIM+1]) * \

70 (1- TRANSACTION_FEE_PERCENT)

71

72 self.state[index+STOCK_DIM+1] -= min(abs(action), self.state[index+STOCK_DIM+1])

73 self.cost +=self.state[index+1]*min(abs(action),self.state[index+STOCK_DIM+1]) * \

74 TRANSACTION_FEE_PERCENT

75 self.trades+=1

76 else:

77 pass

78 else:

79 # if turbulence goes over threshold, just clear out all positions

80 if self.state[index+STOCK_DIM+1] > 0:

81 #update balance

82 self.state[0] += self.state[index+1]*self.state[index+STOCK_DIM+1]* \

83 (1- TRANSACTION_FEE_PERCENT)

84 self.state[index+STOCK_DIM+1] =0

85 self.cost += self.state[index+1]*self.state[index+STOCK_DIM+1]* \

86 TRANSACTION_FEE_PERCENT

87 self.trades+=1

88 else:

89 pass

90

91 def _buy_stock(self, index, action):

92 # perform buy action based on the sign of the action

93 if self.turbulence< self.turbulence_threshold:

94 available_amount = self.state[0] // self.state[index+1]

95 # print('available_amount:{}'.format(available_amount))

96

97 #update balance

98 self.state[0] -= self.state[index+1]*min(available_amount, action)* \

99 (1+ TRANSACTION_FEE_PERCENT)

100

101 self.state[index+STOCK_DIM+1] += min(available_amount, action)

102

103 self.cost+=self.state[index+1]*min(available_amount, action)* \

104 TRANSACTION_FEE_PERCENT

105 self.trades+=1

106 else:

107 # if turbulence goes over threshold, just stop buying

108 pass

109

110 def step(self, actions):

111 # print(self.day)

112 self.terminal = self.day >= len(self.df.index.unique())-1

113 # print(actions)

114

115 if self.terminal:

116 plt.plot(self.asset_memory,'r')

117 plt.savefig('account_value_trade.png')

118 plt.close()

119

120 df_date = pd.DataFrame(self.date_memory)

121 df_date.columns = ['datadate']

122 df_date.to_csv('df_date.csv')

123

124

125 df_actions = pd.DataFrame(self.actions_memory)

126 df_actions.columns = self.data.tic.values

127 df_actions.index = df_date.datadate

128 df_actions.to_csv('df_actions.csv')

129

130 df_total_value = pd.DataFrame(self.asset_memory)

131 df_total_value.to_csv('account_value_trade.csv')

132 end_total_asset = self.state[0]+ \

133 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):(STOCK_DIM*2+1)]))

134 print("previous_total_asset:{}".format(self.asset_memory[0]))

135

136 print("end_total_asset:{}".format(end_total_asset))

137 print("total_reward:{}".format(self.state[0]+sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):61]))- self.asset_memory[0] ))

138 print("total_cost: ", self.cost)

139 print("total trades: ", self.trades)

140

141 df_total_value.columns = ['account_value']

142 df_total_value['daily_return']=df_total_value.pct_change(1)

143 sharpe = (252**0.5)*df_total_value['daily_return'].mean()/ \

144 df_total_value['daily_return'].std()

145 print("Sharpe: ",sharpe)

146

147 df_rewards = pd.DataFrame(self.rewards_memory)

148 df_rewards.to_csv('account_rewards_trade.csv')

149

150 # print('total asset: {}'.format(self.state[0]+ sum(np.array(self.state[1:29])*np.array(self.state[29:]))))

151 #with open('obs.pkl', 'wb') as f:

152 # pickle.dump(self.state, f)

153

154 return self.state, self.reward, self.terminal,{}

155

156 else:

157 # print(np.array(self.state[1:29]))

158 self.date_memory.append(self.data.datadate.unique())

159

160 #print(self.data)

161 actions = actions * HMAX_NORMALIZE

162 if self.turbulence>=self.turbulence_threshold:

163 actions=np.array([-HMAX_NORMALIZE]*STOCK_DIM)

164 self.actions_memory.append(actions)

165

166 #actions = (actions.astype(int))

167

168 begin_total_asset = self.state[0]+ \

169 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):(STOCK_DIM*2+1)]))

170 #print("begin_total_asset:{}".format(begin_total_asset))

171

172 argsort_actions = np.argsort(actions)

173 #print(argsort_actions)

174

175 sell_index = argsort_actions[:np.where(actions < 0)[0].shape[0]]

176 buy_index = argsort_actions[::-1][:np.where(actions > 0)[0].shape[0]]

177

178 for index in sell_index:

179 # print('take sell action'.format(actions[index]))

180 self._sell_stock(index, actions[index])

181

182 for index in buy_index:

183 # print('take buy action: {}'.format(actions[index]))

184 self._buy_stock(index, actions[index])

185

186 self.day += 1

187 self.data = self.df.loc[self.day,:]

188 self.turbulence = self.data['turbulence'].values[0]

189 #print(self.turbulence)

190 #load next state

191 # print("stock_shares:{}".format(self.state[29:]))

192 self.state = [self.state[0]] + \

193 self.data.adjcp.values.tolist() + \

194 list(self.state[(STOCK_DIM+1):(STOCK_DIM*2+1)]) + \

195 self.data.macd.values.tolist() + \

196 self.data.rsi.values.tolist()

197

198 end_total_asset = self.state[0]+ \

199 sum(np.array(self.state[1:(STOCK_DIM+1)])*np.array(self.state[(STOCK_DIM+1):(STOCK_DIM*2+1)]))

200

201 #print("end_total_asset:{}".format(end_total_asset))

202

203 self.reward = end_total_asset - begin_total_asset

204 self.rewards_memory.append(self.reward)

205

206 self.reward = self.reward * REWARD_SCALING

207

208 self.asset_memory.append(end_total_asset)

209

210 return self.state, self.reward, self.terminal, {}

211

212 def reset(self):

213 self.asset_memory = [INITIAL_ACCOUNT_BALANCE]

214 self.day = 0

215 self.data = self.df.loc[self.day,:]

216 self.turbulence = 0

217 self.cost = 0

218 self.trades = 0

219 self.terminal = False

220 #self.iteration=self.iteration

221 self.rewards_memory = []

222 self.actions_memory=[]

223 self.date_memory=[]

224 #initiate state

225 self.state = [INITIAL_ACCOUNT_BALANCE] + \

226 self.data.adjcp.values.tolist() + \

227 [0]*STOCK_DIM + \

228 self.data.macd.values.tolist() + \

229 self.data.rsi.values.tolist()

230

231 return self.state

232

233 def render(self, mode='human',close=False):

234 return self.state

235

236

237 def _seed(self, seed=None):

238 self.np_random, seed = seeding.np_random(seed)

239 return [seed]

Step 5: Implement DRL Algorithms¶

The implementation of the DRL algorithms are based on OpenAI Baselines and Stable Baselines. Stable Baselines is a fork of OpenAI Baselines, with a major structural refactoring, and code cleanups.

Step 5.1: Training data split: 2009-01-01 to 2018-12-31

1def data_split(df,start,end):

2 """

3 split the dataset into training or testing using date

4 :param data: (df) pandas dataframe, start, end

5 :return: (df) pandas dataframe

6 """

7 data = df[(df.datadate >= start) & (df.datadate < end)]

8 data=data.sort_values(['datadate','tic'],ignore_index=True)

9 data.index = data.datadate.factorize()[0]

10 return data

Step 5.2: Model training: DDPG

1## tensorboard --logdir ./multiple_stock_tensorboard/

2# add noise to the action in DDPG helps in learning for better exploration

3n_actions = env_train.action_space.shape[-1]

4param_noise = None

5action_noise = OrnsteinUhlenbeckActionNoise(mean=np.zeros(n_actions), sigma=float(0.5) * np.ones(n_actions))

6

7# model settings

8model_ddpg = DDPG('MlpPolicy',

9 env_train,

10 batch_size=64,

11 buffer_size=100000,

12 param_noise=param_noise,

13 action_noise=action_noise,

14 verbose=0,

15 tensorboard_log="./multiple_stock_tensorboard/")

16

17## 250k timesteps: took about 20 mins to finish

18model_ddpg.learn(total_timesteps=250000, tb_log_name="DDPG_run_1")

Step 5.3: Trading

Assume that we have $1,000,000 initial capital at 2019-01-01. We use the DDPG model to trade Dow jones 30 stocks.

Step 5.4: Set turbulence threshold

Set the turbulence threshold to be the 99% quantile of insample turbulence data, if current turbulence index is greater than the threshold, then we assume that the current market is volatile

1insample_turbulence = dow_30[(dow_30.datadate<'2019-01-01') & (dow_30.datadate>='2009-01-01')]

2insample_turbulence = insample_turbulence.drop_duplicates(subset=['datadate'])

Step 5.5: Prepare test data and environment

1# test data

2test = data_split(dow_30, start='2019-01-01', end='2020-10-30')

3# testing env

4env_test = DummyVecEnv([lambda: StockEnvTrade(test, turbulence_threshold=insample_turbulence_threshold)])

5obs_test = env_test.reset()

Step 5.6: Prediction

1def DRL_prediction(model, data, env, obs):

2 print("==============Model Prediction===========")

3 for i in range(len(data.index.unique())):

4 action, _states = model.predict(obs)

5 obs, rewards, dones, info = env.step(action)

6 env.render()

Step 6: Backtest Our Strategy¶

For simplicity purposes, in the article, we just calculate the Sharpe ratio and the annual return manually.

1def backtest_strat(df):

2 strategy_ret= df.copy()

3 strategy_ret['Date'] = pd.to_datetime(strategy_ret['Date'])

4 strategy_ret.set_index('Date', drop = False, inplace = True)

5 strategy_ret.index = strategy_ret.index.tz_localize('UTC')

6 del strategy_ret['Date']

7 ts = pd.Series(strategy_ret['daily_return'].values, index=strategy_ret.index)

8 return ts

Step 6.1: Dow Jones Industrial Average

1def get_buy_and_hold_sharpe(test):

2 test['daily_return']=test['adjcp'].pct_change(1)

3 sharpe = (252**0.5)*test['daily_return'].mean()/ \

4 test['daily_return'].std()

5 annual_return = ((test['daily_return'].mean()+1)**252-1)*100

6 print("annual return: ", annual_return)

7

8 print("sharpe ratio: ", sharpe)

9 #return sharpe

Step 6.2: Our DRL trading strategy

1def get_daily_return(df):

2 df['daily_return']=df.account_value.pct_change(1)

3 #df=df.dropna()

4 sharpe = (252**0.5)*df['daily_return'].mean()/ \

5 df['daily_return'].std()

6

7 annual_return = ((df['daily_return'].mean()+1)**252-1)*100

8 print("annual return: ", annual_return)

9 print("sharpe ratio: ", sharpe)

10 return df

Step 6.3: Plot the results using Quantopian pyfolio

Backtesting plays a key role in evaluating the performance of a trading strategy. Automated backtesting tool is preferred because it reduces the human error. We usually use the Quantopian pyfolio package to backtest our trading strategies. It is easy to use and consists of various individual plots that provide a comprehensive image of the performance of a trading strategy.

1%matplotlib inline

2with pyfolio.plotting.plotting_context(font_scale=1.1):

3 pyfolio.create_full_tear_sheet(returns = DRL_strat,

4 benchmark_rets=dow_strat, set_context=False)